September 2024 Market Snapshot – the low number of home sales & hurry up to get pictures before snow flies!

Hey, it’s not too late to get stunning exterior pictures of your home—for FREE! With fall just around the corner, now’s the perfect time to capture its beauty before the leaves fall and snow arrives. We’ve been busy lately, taking aerial shots for several homes, and have room for a few more! If yo

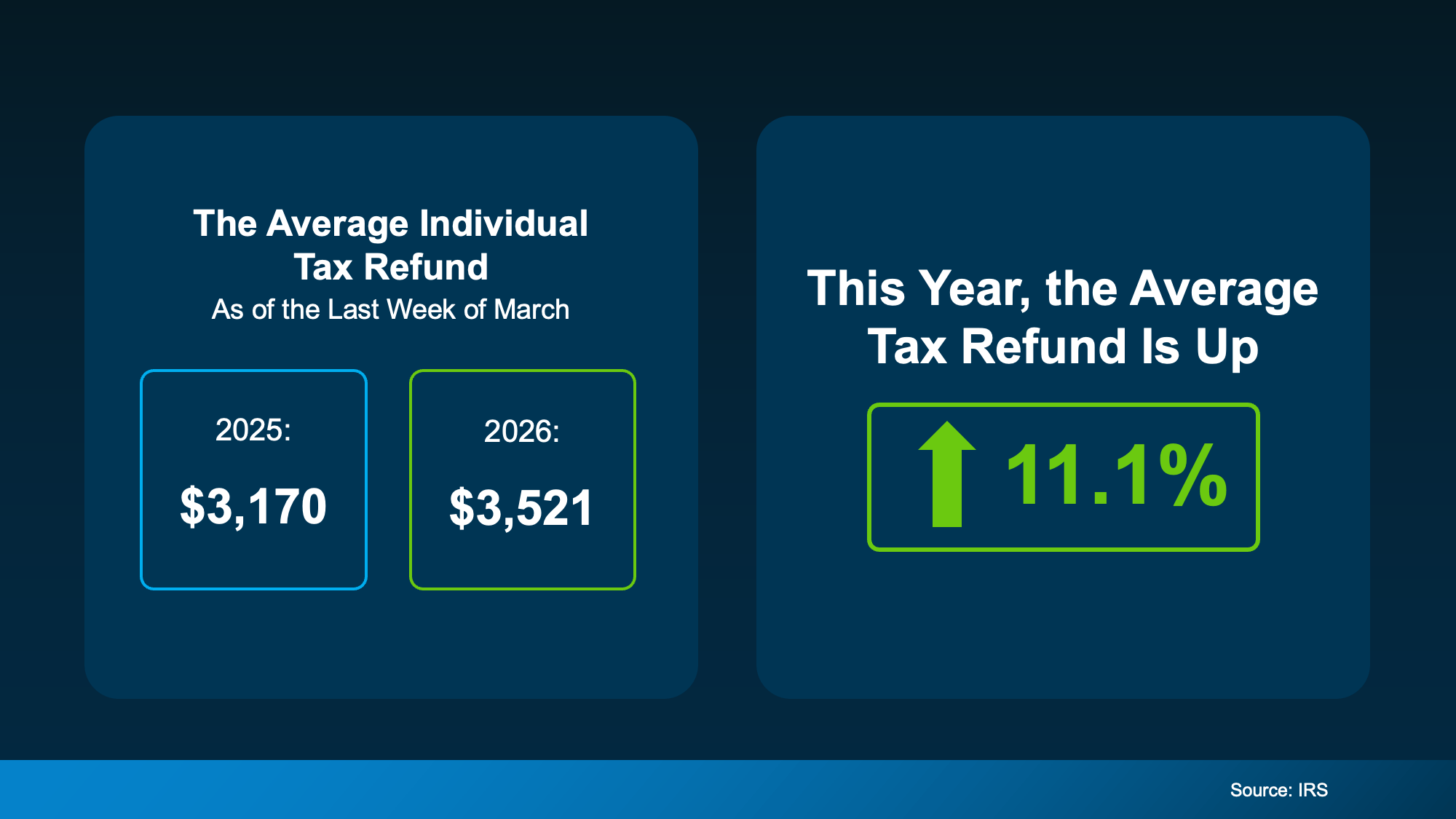

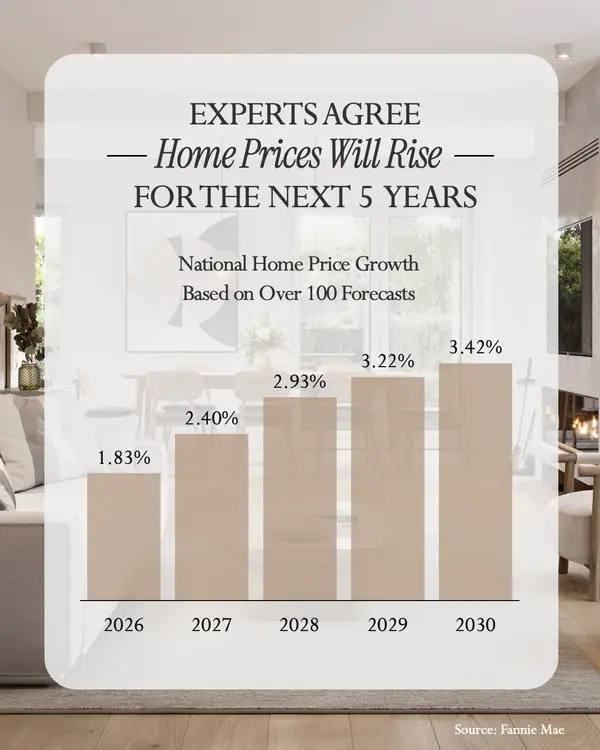

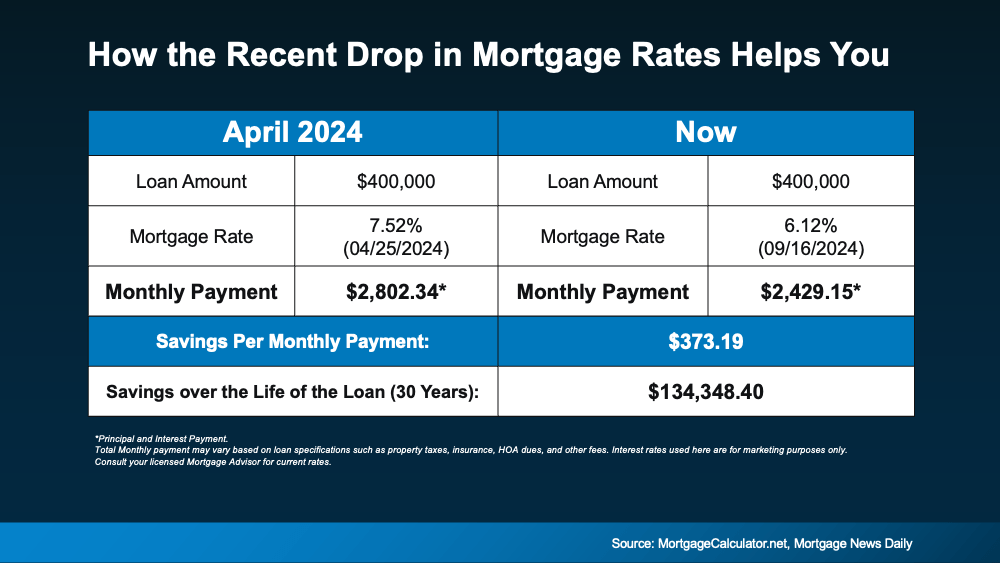

Mortgage Rates Drop to Lowest Level in over a Year and a Half

Mortgage rates have hit their lowest point in over a year and a half. And that’s big news if you’ve been sitting on the homebuying sidelines waiting for this moment. Even a small decline in rates could help you get a better monthly payment than you would expect on your next home. And the drop that’s

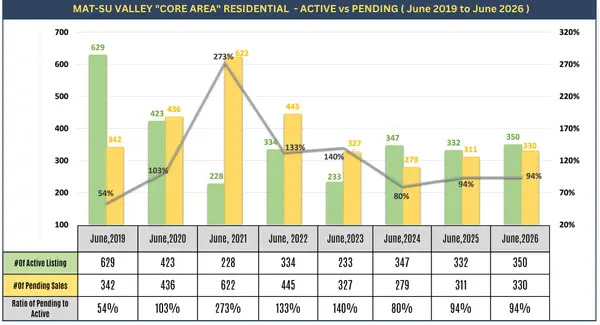

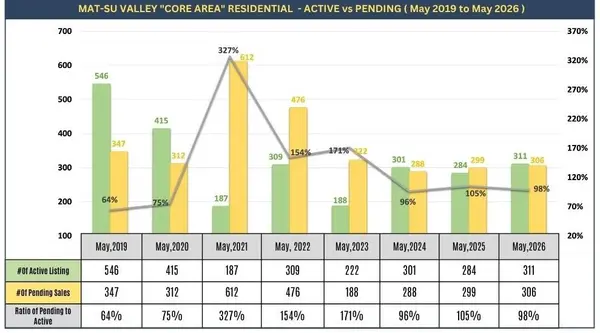

August 2024 Matsu Valley “CORE” Area Residential Market Update from Dave & Travis!

It’s that time of year again! For the last 4 years we have been taking drone/exterior pictures for anyone that might be selling before next Summer. It’s the perfect opportunity to showcase your home’s exterior beauty before the leaves fall and the snow arrives. These stunning aerial shots will high

Categories

Recent Posts