Why Spring Sellers Have the Edge — Insights from Dave & Travis

Spring Sellers Have an Edge. Here’s Why.Homeowners looking to sell usually want three things: plenty of interested buyers, strong offers, and a short timeline. Spring is the season that most often delivers all three.So, if a move has been on your mind this year, this is the window where momentum ten

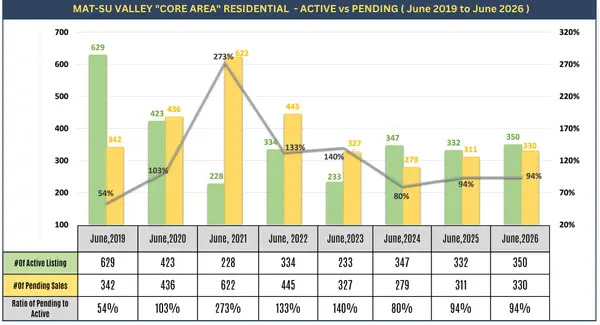

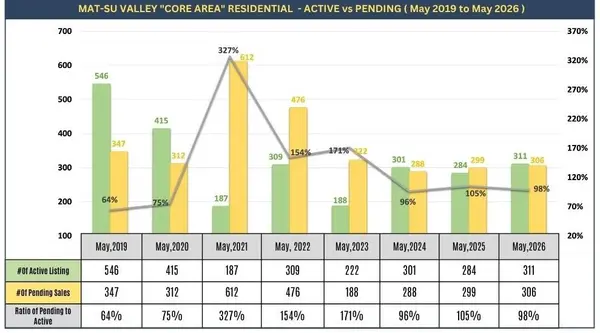

Mat-Su February 2026 Market Update & Smart Planning for Where You’ll Live As You Age - Insights from Dave & Travis

Mat-Su Valley February 2026 Market UpdateI want to share a clear snapshot of what’s happening right now in the Mat-Su “Core Area” market and more importantly, what it means for you if you’re thinking about buying or selling this year. I’ve been tracking February numbers going back to 2019, and the

Estate Planning Insight: Protect Your Assets and Your Loved Ones

I hope your week’s going great! Before we jump into real estate updates, I want to share something important, something that directly impacts your home, your finances, and the people you care about most.A while back, I came across an eye-opening article by Tayva Taylor from Alaska Law & Mediation

Categories

Recent Posts